Today, I want to talk about a stock I’ve been buying recently, Cameco (CCJ). I’ve traded it multiple times over the past 2 to 3 years, and now I’m getting back into it.

So what’s the deal with Cameco? It’s a big player in the nuclear uranium space, with a market cap of $13 billion and a share price just below $31. Long-term, nuclear power helps cut global carbon emissions. Since 2020, the uranium supply-demand situation has balanced out after a decade of building inventories.

Last year, uranium prices got stronger due to obvious reasons, and this trend continues into this year. Cameco scored a huge contract worth $4 billion to supply uranium to Ukraine, their largest ever. In their Q1 report, the CEO highlighted the soaring demand for nuclear power.

Cameco operates in two major areas: uranium production and fuel services. They’re a major player in mining and refining uranium, operating in a stable part of the world. They’re the top North American uranium miner and second globally. Their products are crucial for clean electricity generation in nuclear power plants worldwide.

Their competitive edge lies in owning the world’s largest high-grade reserves mine and having low operational costs. They’re among the few capable of meeting uranium demand globally. Utilities prefer reliable suppliers like Cameco to avoid risking nuclear reactor shutdowns due to fuel shortages.

The company is experiencing robust earnings growth, over 200% this year, though from a low base. Earnings are expected to rise to $1.03 this year and even more the next. Currently, the stock trades at a PE ratio of 30 times this year and 18 times next year, with almost no short interest.

The long-term story here is the expanding role of nuclear energy globally, driven by the need to meet ambitious carbon emission goals. Governments, including the US, are supporting the nuclear industry. Supply and demand in the uranium market have been balancing out since 2020, exacerbated by the Russian-Ukrainian conflict.

The uranium market operates on a long cycle, taking up to ten years to develop a mine or build a nuclear reactor. Fukushima in 2011 marked the low point of the cycle, and now, a decade later, it’s poised for a reversal. Uranium demand is rising, with about 50 reactors under construction, compared to 440 in operation a couple of summers ago.

The number of nuclear power users is set to increase, especially in places like China and India. Producers have become consumers, boosting uranium prices. Supply is insufficient due to natural degradation of mines over time.

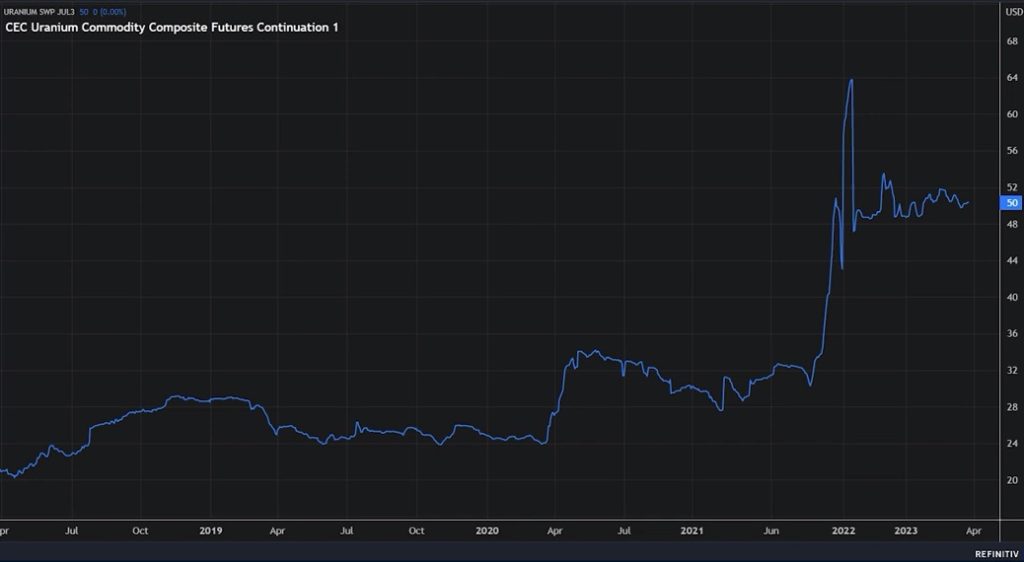

Miners may need $60/lb uranium to increase capacity to meet demand. Current price is around $50/lb. Cameco could see a significant increase. In 2007, Cameco was valued at $20 billion; now it’s over $12 billion.

Good supply-demand dynamics favor uranium suppliers. The industry has been in a bear market, likely past the major turning point. Recent developments include acquiring Westinghouse Electric and restarting a high-grade uranium mine.

Cameco has a contract with Ukraine worth $4 billion to supply uranium, reducing reliance on Russian fuel. There’s potential for other East European countries to follow suit. CEO is bullish on nuclear power demand.

A bill to fast-track advanced nuclear reactors deployment was advanced in the US Senate. This affects the sector positively. Investing in uranium ETFs is another option. EPS increased by 8% in Q1.

Next earnings report expected in July. Stock could easily trade up into the mid-thirties. I’m accumulating shares.